Dados Econômicos

O dado mais importante da semana foi a divulgação do IPCA de junho, o qual veio consideravelmente baixo, em 0,15%. A Anbima projetava 0,33%, veio menos da metade. Com isso o acumulado em 12 meses ficou em 4,64%. Me chamou a atenção como o índice de difusão veio baixo, em apenas 53,60%, mostrando uma inflação bem concentrada, o que foi o caso, ficando na parte habitacional. Se a bandeira tarifária de energia tivesse alterado de amarela para verde, possivelmente a inflação seria ainda mais baixa.

Também foi divulgada a primeira prévia do IGPM de julho, o qual veio negativo em -0,39%, o que parece reforçar a expectativa de um índice negativo no mês de julho. A Anbima projeta um índice negativo em 0,71%.

Os dois índices se comunicam no sentido de que suas quedas decorrem muito da queda no petróleo em razão do fim da guerra no Oriente Médio, a qual acabou sendo retomada nos últimos dias, fazendo o petróleo voltar a subir. Apesar disso, a alta do petróleo não foi tão elevada a ponto de gerar, ainda, impactos na inflação novamente.

Esse é o último IPCA antes da próxima reunião do Copom, o que deve facilitar um pouco a decisão por um possível novo corte de 25 bps, como venho achando mais provável (dois cortes de 25 bps nas próximas duas reuniões).

O IPCA foi divulgado na sexta-feira e parece que o mercado se empolgou um pouco, ações e FIIs tiveram uma valorização; no entanto, ainda vemos a NTNB 2040 em patamares muito elevados, tendo fechado em 7,53%. Esse patamar elevado vai seguir pressionando as cotas da renda variável, o que tem me feito segurar um pouco novos investimentos, mas isso precisa ser tratado com base na estratégia de cada investidor. Tratarei mais deste tema no próximo relatório.

Juros, cap rate e um possível efeito futuro das compras com cotas nos FIIs

Ao longo da análise do TVRI11 desta semana, ao comentar o trecho do relatório gerencial em que o fundo destaca a reavaliação do portfólio, com resultado negativo de 4% e redução do valor patrimonial, essa observação pontual acabou puxando uma reflexão mais ampla, que na verdade vale para toda a indústria de FIIs e para o mercado imobiliário como um todo. Por isso, em vez de deixar restrita ao tópico do TVRI11, trago essa reflexão para a abertura do relatório desta semana.

Imóveis de renda são avaliados majoritariamente pelo método em que o avaliador projeta o fluxo de aluguéis do ativo e o desconta a uma taxa que reflete o custo de oportunidade do capital, construída a partir do juro real da economia, a NTN-B, mais um prêmio de risco pelo ativo. Com a curva de juro real aberta (ou seja, elevada), essa taxa de desconto sobe, e o mesmo fluxo de aluguéis passa a valer menos a valor presente. Um exemplo para ficar mais claro: um imóvel com NOI anual de R$ 100 avaliado a uma taxa de capitalização de 8% vale R$ 1.250. O mesmo imóvel, com o mesmo NOI, avaliado a 10% vale R$ 1.000, uma redução de 20% no valor do ativo sem qualquer alteração na receita. É essa mecânica que explica a variação média de -4,00% nos laudos do TVRI11 e a pressão sobre os VPs dos fundos de tijolo em geral neste ciclo. O movimento inverso vale igualmente: quando o juro real cede, a taxa de capitalização exigida comprime, e o valor presente do mesmo fluxo de aluguéis sobe. É o ciclo imobiliário operando pela taxa de desconto, não pelo tijolo.

Esse parêntese conversa com um ponto que venho repetindo sobre os fundos que estão adquirindo imóveis pagos com cotas neste momento do ciclo. O ativo entra no portfólio avaliado com a taxa de capitalização atual, que está próxima do topo histórico, e com o cap rate de entrada da aquisição travado sobre a renda contratada. Mesmo nas compras via emissão de cotas, e mesmo quando o preço sai um pouco acima da média da região, sigo enxergando racionalidade nessas aquisições: o fundo carrega renda contratada a cap rates elevados e trava o preço de compra num momento em que a taxa de desconto está no ponto mais alto do ciclo. Quando o juro real ceder, os laudos passarão a descontar o mesmo fluxo a taxas menores, o valor de avaliação dos imóveis sobe e o VP do fundo acompanha, sem depender de qualquer ação da gestão além do carrego do ativo. A compressão de cap rate, que hoje joga contra os laudos, passa a jogar a favor. Mas, claro, não sejamos inocentes, algumas compras com trocas de cotas podem ser ruins, com trocas de favores, e não gerar este potencial de valorização, para isso fazemos análises, e acima de tudo, diversificamos.

E já que eu abri um parêntese para explicar esse detalhe pontual de como funciona a precificação dos imóveis dentro de um ciclo imobiliário, vale aproveitar essa mecânica para tentar antecipar um cenário para o mercado de FIIs, especificamente para os fundos que estão comprando imóveis pagando em cotas. Temos visto vários fundos nesse movimento, com destaque para TRXF11 e GGRC11, mas não se restringindo a eles.

O ponto é o seguinte: se essas aquisições via emissão de cotas continuarem por um período longo, e se mais fundos seguirem esse caminho, vale a pena projetar o que pode acontecer quando o cenário econômico virar, ou seja, quando a atividade melhorar e os juros cederem.

O primeiro efeito, como já descrevi, é o VP subindo à medida que os laudos anuais de reavaliação incorporarem taxas de capitalização menores. O ponto que quero acrescentar é que esse efeito provavelmente não deverá aparecer de imediato na cotação em bolsa, e o motivo está do outro lado dessas transações. Os vendedores que hoje aceitam vender no ciclo baixo do mercado, muitas vezes recebendo em cotas, ficam então segurando uma posição relevante nesses fundos, talvez com um período de lock-up contratual antes de poder negociá-la ou apenas aguardando um cenário melhor para venda. Numa melhora do cenário econômico, esses mesmos vendedores tendem a querer transformar essa posição em caixa novamente, seja para reinvestir em novos negócios, seja para simplesmente realizar o ganho. Isso significa colocar um volume grande de cotas à venda no mercado secundário.

Esse fluxo vendedor tende a pressionar a cotação justamente no momento em que o VP está subindo, ampliando o desconto entre VM e VP por um tempo. Com isso, a percepção de desconto entre os investidores vai ficando maior, mas ainda sem vermos valorização nessas cotas em razão da alta pressão vendedora. Ou seja, como uma mola sendo comprimida. É um desalinhamento temporário entre o valor patrimonial, que reflete o valor dos ativos, e o valor de mercado, que reflete a oferta e demanda por cotas no curto prazo. Só quando esse estoque de cotas for absorvido pelo mercado, seja por novos compradores atraídos pelo desconto crescente, seja pelo próprio fundo recomprando cotas abaixo do VP, é que a cotação tende a andar para cima de forma mais rápida, soltando a mola de uma vez. Historicamente, esse tipo de movimento de descompressão tende a ser mais abrupto do que gradual, porque o gatilho costuma ser uma mudança de percepção de mercado, não uma reprecificação lenta. Nesse caso, ocorreria a retirada de uma parede que segurava a cotação.

Depois dessa fase, entra um segundo efeito, mais estrutural. Fundos que compraram imóveis nesse ciclo de baixa, e que já estarão com esses ativos reavaliados para cima, ganham a possibilidade de vender esses mesmos imóveis num mercado mais aquecido, com mais liquidez, prazos de venda mais curtos e preços melhores. Isso tende a gerar ganhos de capital relevantes, e consequentemente uma onda de rendimentos não recorrentes elevados, que pode se estender por vários meses ou até anos, dependendo do volume de aquisições feitas via cotas nesse período, do ritmo de desinvestimento que a gestão escolher e do número de parcelas a receber dessas vendas.

Esse tipo de ciclo, onde o não recorrente sobe de forma consistente por um período prolongado, costuma ser um dos momentos mais importantes para o cotista pensar em reinvestimento. É justamente nesse tipo de janela, com caixa entrando de forma mais robusta que o normal, que fica mais fácil proteger o capital contra a inflação futura, recompondo posição a preços que o próprio ciclo ajudou a formar. Só que aqui aumentamos o risco de uma valorização excessiva das cotas por investidores que não sabem diferenciar rendimento recorrente de não recorrente, momento que também precisa de atenção para o reinvestimento.

Importante, isso se trata apenas de um exercício de cenário, não de uma previsão com data marcada, o timing exato depende da trajetória dos juros e de quando, de fato, os vendedores de hoje decidirem monetizar suas posições. Como eu costumo dizer, precisamos entender a dinâmica do que pode ou não acontecer e, caso ocorra, conseguimos interpretar de forma mais rápida.

Fica então o quadro completo do ciclo, do ponto de vista de quem compra hoje aceitando cotas como moeda de troca. Primeiro, o VP sobe pelos laudos, sem que a cotação em bolsa acompanhe no mesmo ritmo, justamente pela pressão vendedora de quem recebeu cotas e quer transformá-las em caixa. Depois, à medida que esse estoque de cotas for absorvido, a cotação recupera terreno de forma mais rápida do que subiu o VP. E por fim, esses mesmos fundos, já de posse de imóveis comprados na baixa e reavaliados na alta, encontram janela para vender com ganho, alimentando uma fase de rendimento não recorrente elevado. São três movimentos concatenados, mas que não acontecem no mesmo tempo nem na mesma velocidade, e nenhum deles depende de uma ação isolada da gestão, dependem principalmente da direção dos juros e do apetite dos vendedores de cotas em cada etapa. Para o cotista de longo prazo, entender essa sequência ajuda a não estranhar descontos abrindo justamente quando os fundamentos estão melhorando, e a se posicionar com antecedência para aproveitar tanto a descompressão da cotação quanto o não recorrente que deve vir depois dela.

Fonte: Desmistificando Research

Evidentemente que agora precisamos de um acompanhamento para saber o desdobramento de tudo isso, mas sim, quanto mais tempo os juros ficam elevados, mais a mola pode ser comprimida.

E isso não acontece só nos FIIs de tijolo, mas em todos os FIIs, como passo a analisar agora nos FIIs de recebíveis e o impacto na visualização do desconto P/VP.

Descontos sobre o valor patrimonial do IFIX – uma visão que não podemos perder

Esta semana um amigo me enviou um gráfico sobre o histórico de negociação do IFIX em relação ao VP ao longo dos anos, mostrando que temos um desconto médio relevante do ponto de vista histórico, mas não tão grande.

É sempre um gráfico interessante de olharmos e nos mostra como os FIIs estão descontados e nós vemos isso pelo preço que esses fundos negociam.

Só que eu chamei a atenção dele para um ponto e aproveito para fazer o mesmo com os nossos assinantes.

Quando olhamos para a história do IFIX, ele no passado sempre foi muito concentrado em tijolo, passando cada vez mais a ter FIIs de recebíveis depois de 2020, tendo quase 50% do IFIX nesta classe de ativos no momento.

E quando eu olho para isso, eu preciso entender como os VPs desses fundos são pressionados ou possuem potencial de valorização, quando estamos com os juros tão elevados por muito tempo.

Uma forma de demonstrar visualmente isso é olharmos para o relatório de KNIP11 de 2022 e de hoje. Se olharmos o relatório do fundo de janeiro de 2022 temos a seguinte foto:

Fonte: https://fnet.bmfbovespa.com.br/fnet/publico/exibirDocumento?id=261761&cvm=true

O “yield médio curva” é por quanto o CRI foi comprado e ele será o responsável por colocar dinheiro no nosso bolso no formato de rendimentos. O “yield médio MTM” é o quanto o VP eventualmente caiu referente ao que foi comprado, mostrando um potencial de valorização do VP para voltar aos preços adquiridos, seja por uma queda do juro, seja pelo vencimento dos títulos.

Vejam a diferença entre um e outro em 2022.

Agora, observem a diferença para hoje:

Fonte: https://fnet.bmfbovespa.com.br/fnet/publico/exibirDocumento?id=1242372&cvm=true

Aqui os nomes mudaram, mas são a mesma coisa. A taxa média de aquisição subiu, pois na medida que os títulos vencem e novos são comprados, essa taxa sobe, aumentando o potencial de rendimentos. E isso é um ponto relevante, pois quanto maior for, maior o potencial de valorização no futuro.

Agora observe a taxa MTM. Observe a diferença entre essa taxa e a de aquisição, comparando com a diferença em 2022.

Isso significa que o VP teve uma boa desvalorização frente aos valores pagos pelos títulos.

Não entrarei nos vários detalhes que seriam necessários para entender esses indicadores e vou ficar restrito ao potencial do VP.

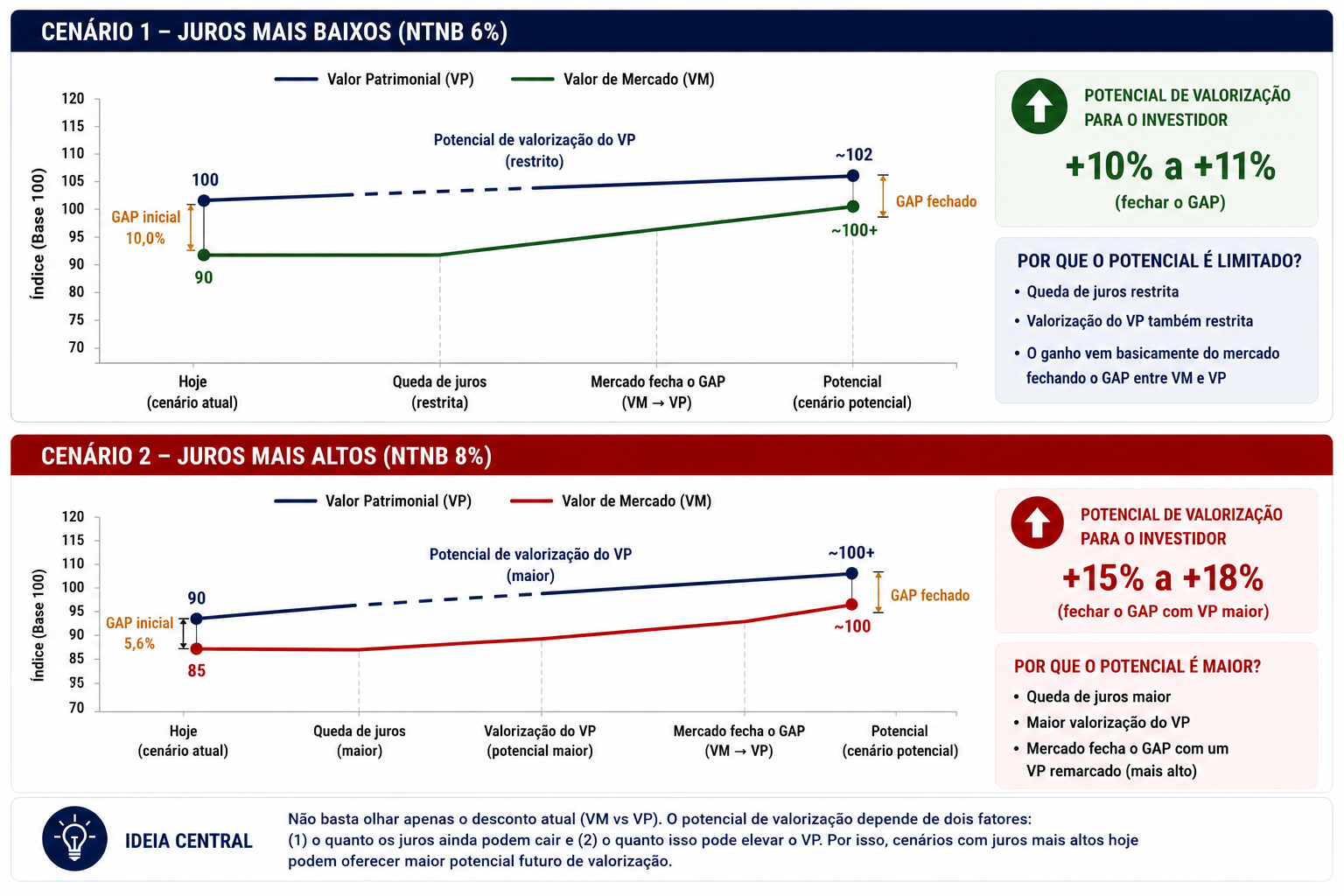

O que pretendo mostrar é o seguinte. Se a NTNB de referência está, por exemplo, em 6%, e temos um VP de um FII a 100 e o seu VM a 90, temos um potencial de valorização de um pouco mais de 10% se o mercado fechar o GAP entre VP e VM, sendo que o potencial de queda de juros é restrito, logo, o potencial de valorização do VP é restrito.

Agora se eu tenho uma NTNB em 8% e o VP deste fundo caiu para 90 e o seu VM é 85, parece que eu tenho um desconto menor neste fundo, pois eu preciso de um pouco mais do que 5% de valorização para retornar para o VP; no entanto, a potencial queda de juros é maior e isso levaria a uma valorização do VP, logo, se o mercado decide fechar o GAP com uma valorização do VP, o potencial de valorização é maior.

Fonte: Desmistificando Research

Ou seja, olhar para essa classe de FIIs e ignorar isso é, por vezes, olhar para o seu indicador histórico e pensar “Ah, nem está tão descontado assim”, quando isso não é verdadeiro.

E temos mais, quanto mais tempo ficamos com juros elevados, como temos tido, mais a renovação da carteira ocorre nesses títulos e maior passa a ser o potencial de valorização do VP.

E sim, isso vale para todas as classes de FIIs, mas captura-se mais rapidamente nos FIIs de recebíveis e nos FoFs/Multiestratégias, os quais não precisam de 1 ano ou mais para fazer as reavaliações de suas propriedades.

Assim, sim, olhemos para indicadores históricos para entendermos os preços de hoje, mas tenhamos o conhecimento necessário para interpretar os números, os quais mostram descontos bem relevantes atualmente.

Cuidado em suas ordens de venda

O mercado de renda variável está de uma forma que poderíamos dizer “estar largado”.

Dizer que está largado parece muito duro e realmente é, mas é uma forma que tenho para chamar a atenção dos assinantes.

Se colocar uma ordem de 100 cotas de base 100, ou seja, “apenas” R$ 10 mil, já aparecem os robôs e parece que será impossível executar a ordem. Se colocar uma ordem maior, do tipo 1.000 cotas de 100, fica uma missão quase impossível fazer negócio.

Isso de certa forma acontece pois estamos há muitos meses com juros elevados e os investidores estão cada vez mais desesperançosos com o mercado de renda variável e a movimentação, por vezes, acaba ocorrendo muito por meio de outros fundos que negociam.

Assim, minha recomendação é, tenham cuidado ao colocar uma ordem de venda, caso esta não seja feita pela visualização de um problema que está se antevendo com urgência.

Quando a venda é feita de forma estratégica ou é feita para se tirar um risco desconfortável, mas ainda distante, evite colocar valores muito abaixo do negociado. Sempre que possível coloque ordens ocultas, ficando aparentes apenas pequenas ordens, como 10 ou 50 cotas. Mas, atenção. Ordens ocultas só podem ser feitas quando não se paga corretagem fixa. Hoje em dia quase nenhuma corretora cobra corretagem de FII, o que faz sentido, mas, caso se pague, deve-se evitar, pois, a cada disparo uma corretagem é cobrada.

Ah, sim, se você opera com banco, dificilmente terá a opção de ordem oculta. Também é conhecida como ordem “iceberg”, na ideia de que uma pequena parte fica visível apenas, e o tamanho maior fica oculto, executando aos poucos.

A depender da situação, vender 1 ou 2 dias antes do rendimento pode ser mais fácil, com mais liquidez. E não se preocupe com a perda do rendimento na sequência, o ajuste feito na data “ex” normalmente corrige isso, fora que é possível ter que vender as cotas por valores mais baixos do que a soma do que você vendeu + rendimentos. Além disso, você pode vender e comprar no mesmo dia outro fundo e garantir o rendimento deste outro, mas, cuidado também, pois pode estar pagando o valor do rendimento já neste preço.

Ah, se você usa bancos, alguns deles não permitem você vender e comprar o ativo no mesmo dia, mas só depois da liquidação da venda, então preste atenção nisso também.

Depois, evite ficar ansioso. Se você não paga corretagem e levar alguns dias para vender, normalmente não há problema. Em geral, a minha experiência nos mostra que ficamos ansiosos, vendemos por qualquer preço, quando se tivéssemos esperado mais tempo o preço poderia ser melhor.

Claro, tudo isso é válido se a venda não ocorre por situações que estamos vislumbrando um problema batendo na porta.

Assim, em tempos de desânimo dos investidores com o mercado de capitais, de juros extremamente elevados e de incertezas que se avolumam, ter um pouco de estratégia e muita paciência vai evitar você ter prejuízos desnecessários.

Obviamente tudo isso vale para as ordens de compra também. Alguém que se arriscar a colocar uma ordem a mercado de 1.000 cotas, em quase qualquer FII, tem o risco de pagar 2% ou 3% mais caro no fundo, quem sabe até a levar a um leilão, tamanha a distorção do preço negociado.

Por isso, aproveite as oportunidades, mas deixe de lado a ansiedade. Faça os giros necessários, mas deixe de lado a ansiedade.

Os FoFs na independência financeira – é possível?

Depois de escrever o texto, decidi inserir este parágrafo inicial. O texto abaixo pode ser um tiro enorme no pé do meu serviço, desestimulando o assinante a não precisar mais dele. Espero que não aconteça, mas a verdade é que isso mostra o nível de independência que busco ter, até mesmo dos nossos próprios interesses, sempre pensando no investidor.

Vamos ao texto.

No começo de 2020 apresentei o meu trabalho de conclusão de MBA no mercado financeiro e o tema era algo que muito me interessava, o uso dos FIIs para a independência financeira.

Foi daí que surgiu a ideia da necessidade de se reinvestir 30% da renda dos FIIs para se poder usar os fundos de forma a pagar as contas; no entanto, infelizmente as pessoas acabam não lendo o texto e saem distorcendo os conceitos que foram discutidos no trabalho.

Quem ainda não teve oportunidade de ler, está disponível em nosso site uma versão em artigo, gratuitamente, no seguinte LINK.

Dito isso, vamos ao motivo deste tópico.

Esta semana eu me perguntei: E se ao invés de ter feito uma carteira diversificada, como no trabalho, tivesse comprado apenas um único FoF ou Multiestratégia?

Para responder essa pergunta, baixei todos os rendimentos e cotações do RINV11 em uma planilha e com a ajuda da IA fiz um exercício do que teria ocorrido, desde o IPO do fundo. Usei o RINV11 pela minha confiança na Gestora.

Fiz dois cenários, ambos como se o investidor tivesse investido no início R$ 100 mil e pudesse comprar cotas fracionárias, para facilitar a conta, mas sem perda de dados.

No cenário 1 eu faço um processo de reinvestimento de 30% de tudo que se ganha, mês a mês, ou seja, gastamos 70% do que se ganhou mês a mês. Essa que é a interpretação errada do meu trabalho. Mas mesmo assim, fiz este exercício.

No cenário 2 eu faço o processo de reinvestimento igual explico no meu trabalho, em que no mês 1 travamos uma renda, algo tipo um “salário”, equivalente a 70% dos rendimentos do fundo e, deste ponto em diante, tudo o que exceder a esta trava é reinvestido obrigatoriamente. Essa trava é corrigida uma vez por ano, a cada 12 meses, pelo IPCA acumulado.

E o resultado é o seguinte.

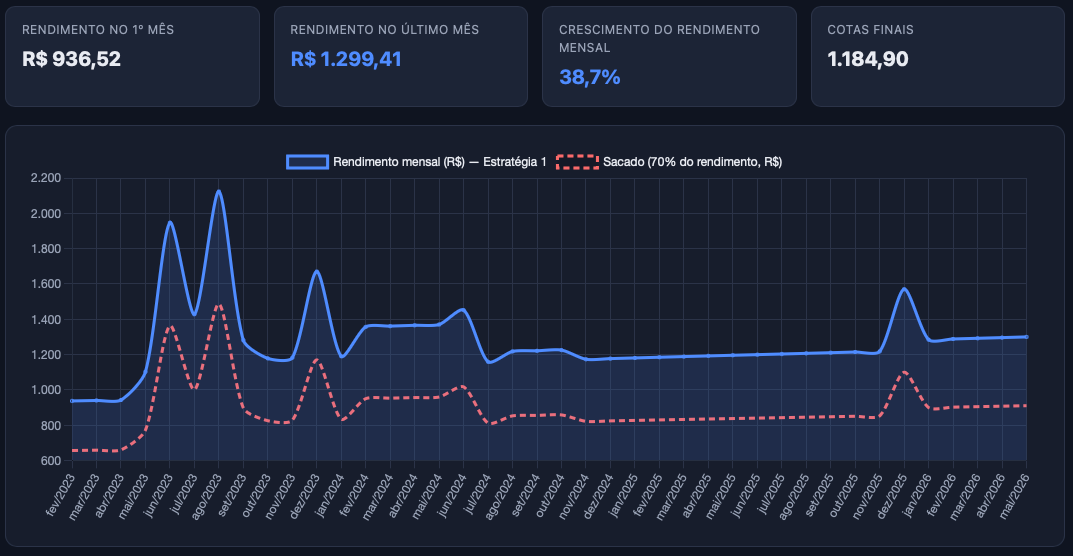

Cenário 1

Fonte: Desmistificando Research

A linha azul é o rendimento total e a linha tracejada os 70%. O rendimento total começa em R$ 936,52 e sobe para R$ 1.299,41. A inflação do período foi de 17,38%, o que precisaria subir a renda para R$ 1.099,37.

Ou seja, ao reinvestir 30% de forma linear o rendimento cresceu bem acima da inflação no período.

Mas tem um problema, se o investidor vivesse dos seus investimentos, ele teria uma situação financeira meio caótica, onde em fevereiro de 2024 poderia gastar R$ 949,00 e em novembro de 2025 poderia gastar R$ 852,00. Na minha visão não tem planejamento financeiro que sobreviva a isso.

É por isso que o método correto, na minha visão, é o cenário 2.

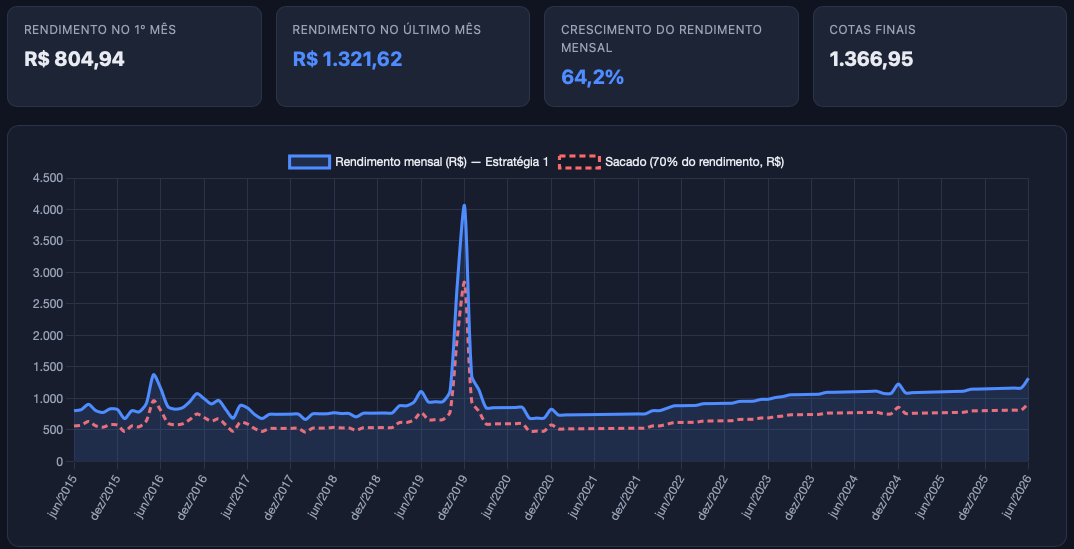

Cenário 2

Fonte: Desmistificando Research

O rendimento inicial, obviamente, é igual, o que muda é o reinvestimento maior, o que faz o último rendimento do estudo ser bem acima da correção pela inflação, de R$ 1.401,33, mesmo a nossa trava corrigindo com a inflação. No longo prazo isso pode não ocorrer de forma obrigatória, como veremos adiante.

Um ponto importante, a trava inicial ainda é um valor considerado extremamente elevado, pois representaria 7,86% do patrimônio total do investidor naquele início. Qualquer pessoa que já tenha lido sobre independência financeira, fala-se entre 4% e 5%.

A importância da trava surge para dar linearidade ao poder de gasto, como podemos ver no mesmo comparativo anterior, onde agora em fevereiro de 2024 pode-se gastar R$ 685,00 e em novembro de 2025 o valor de R$ 716,00.

É claro, neste cenário 2 o poder de gastar é menor que o cenário 1, mas isso é essencial para a sustentabilidade de longo prazo neste caso frente à inflação, pois, como vimos, no cenário 1 há muito mais oscilação. Em um intervalo curto pode parecer que não tem problema, mas em um cenário longo terá, como passamos a ver de agora em diante.

Uma visão mais longa – BCIA11

Depois que eu fiz as reflexões de RINV11, decidi fazer o estudo em um FoF que pudesse ser mais longo e no caso o escolhido foi BCIA11, pois temos uma janela superior a 10 anos e pela confiança que também tenho na equipe do BCIA11.

Mesmos cenários.

Cenário 1

Fonte: Desmistificando Research

Começamos podendo gastar R$ 563,45 (70%), mas vamos gastando sempre 70% do que ganhamos. No final do período, esses R$ 563,45 equivalem a R$ 1.006,62, sendo que 70% do rendimento seria R$ 925,13 e no mês anterior de R$ 817,92, ou seja, não seria suficiente para se viver com a renda dos FIIs crescendo frente à inflação.

Isso, obviamente, é derivado da ideia de se investir 30% do que se ganha e não de criar a trava, logo, neste modelo vive-se uma gangorra e não um planejamento

Mas agora vamos para o cenário 2.

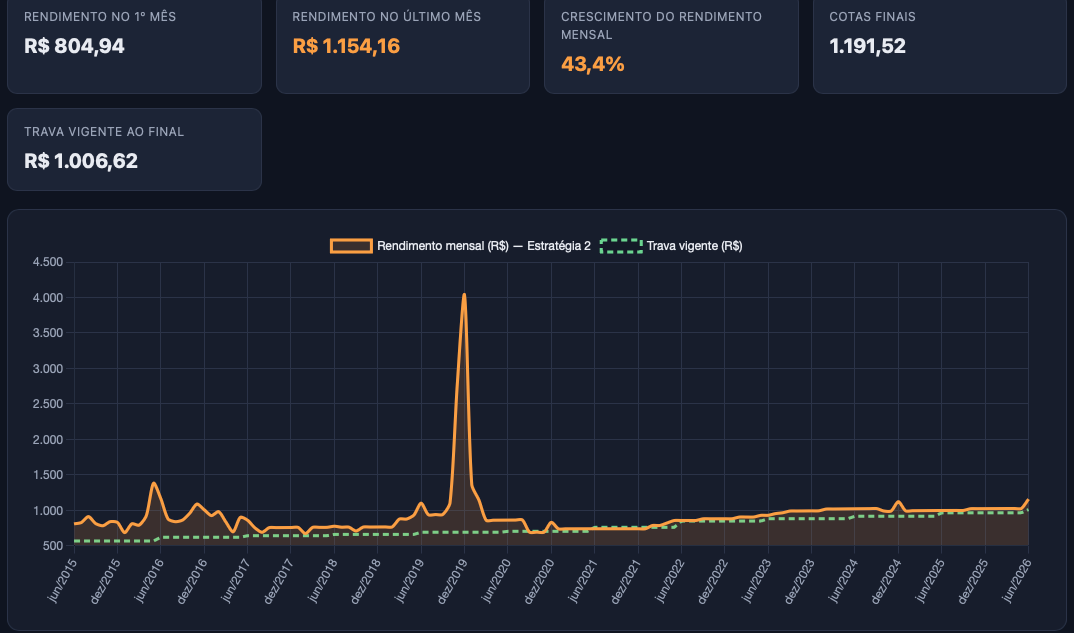

Cenário 2

Fonte: Desmistificando Research

No cenário 2, como podemos ver, a renda da carteira cresce menos. Isso ocorre pelo fato de que o nível de saque é maior ao longo do tempo, reduzindo o reinvestimento.

Neste caso, começamos podendo gastar os mesmos R$ 563,45 e terminamos gastando R$ 1.006,62, sendo que desde meados de 2020 praticamente não reinvestimos.

Ou seja, se o investidor tivesse usado um FoF como BCIA11 nesses 11 anos e aplicado a regra do meu trabalho de conclusão do MBA, teria conseguido retirar valores crescentes frente à inflação, mas estaria chegando no limite do poder de crescimento deste rendimento e precisaria rever a sua estratégia.

Mas, vamos para um ponto importante onde eu sempre explico que é necessário entender o meu TCC. O meu TCC usa FIIs de tijolo em uma época que não se falava quase em ganho não recorrente. Isso é totalmente diferente de um FoF, ou um multiestratégia, ou mesmo os FIIs de tijolo hoje, que costumam ter muito ganho de capital, logo, um yield mais elevado que tínhamos no passado.

Neste cenário 2, o gasto começa em 6,76% do patrimônio, o que é considerado bastante para a ideia da independência financeira.

Assim, decidi fazer um terceiro cenário.

Cenário 3

Fonte: Desmistificando Research

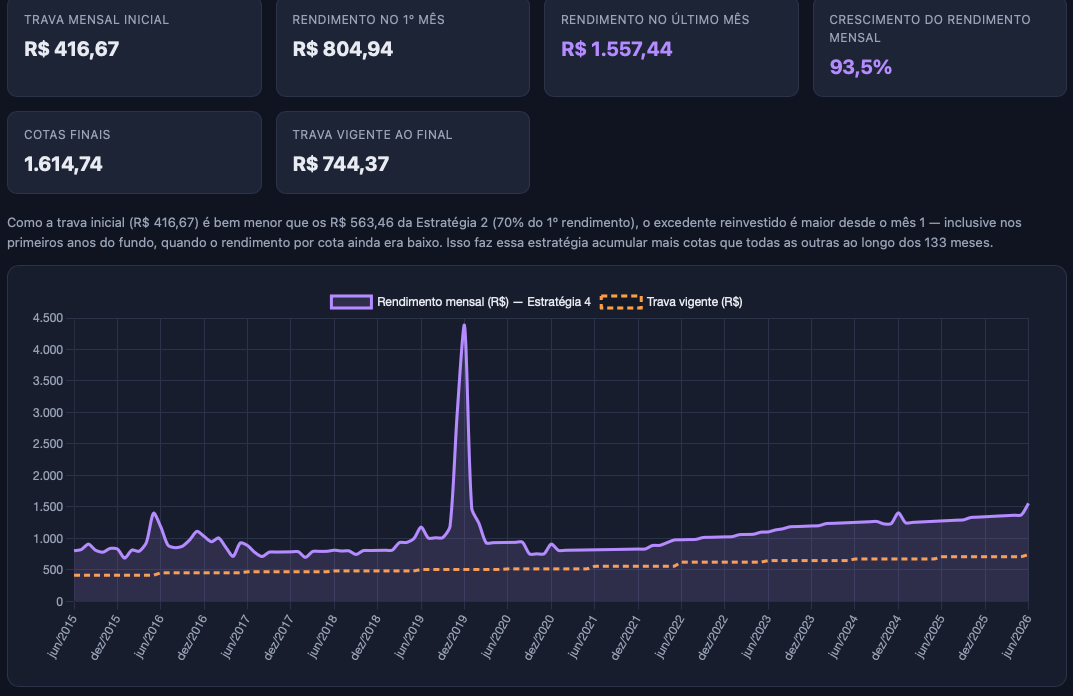

Neste cenário fiz o seguinte, travei a renda inicial, como se fosse o salário, em 5% a.a. do patrimônio, o que nos deu R$ 416,67. Corrigindo pela inflação, ao final do período, precisaríamos de R$ 744,37. O gráfico acima mostra que conseguimos isso com muita facilidade e até aumenta o nosso poder de reinvestimento. Observe, eu travo o “salário” e passo a corrigir ele pela inflação.

Isso é simples, quanto mais eu posso reinvestir e acumular no começo, mais tendo a gerar um bolo que vai passar pelos juros acumulados, melhorando a equação.

Cenário 4

Por fim, decidi fazer um último cenário.

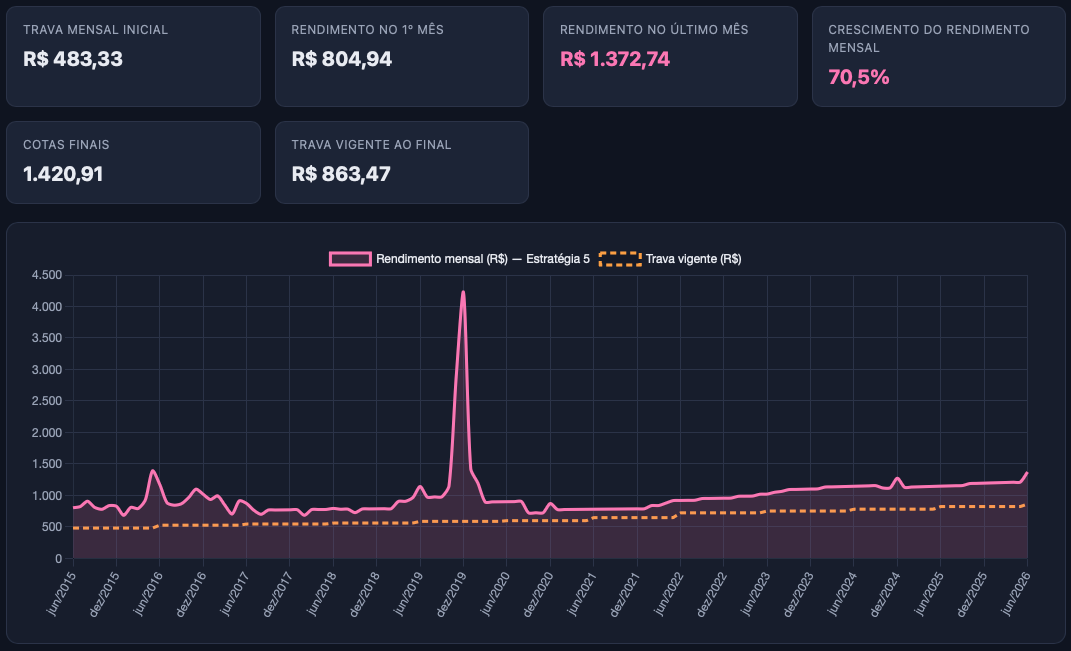

No meu TCC, como eu disse, eu trabalho com uma regra de FIIs de tijolo, que quase não tinham ganho não recorrente, logo, o yield inicial era mais baixo. Isso fez com que iniciássemos a trajetória do estudo gastando 5,80% do patrimônio. Do mesmo jeito, eu travo o “salário”, passo a corrigir pela inflação e reinvisto o excedente.

Decidi aplicar o mesmo nível de saque de 5,80% em BCIA11 e o resultado foi o seguinte:

Fonte: Desmistificando Research

O “salário” inicial agora começa um pouco mais elevado – R$ 483,33 - e no final do período é de R$ 863,47. Como vemos no gráfico, sempre é possível usar o valor proposto e reinvestir, sendo que no atual momento reinveste 37% da renda.

A conta estaria fechando, até o momento, perfeitamente.

Conclusão

Em uma visão simplista, usando principalmente BCIA11, tudo que eu trabalhei no meu TCC continua válido, desde o processo de trava de renda inicial, quanto ao nível de renda mensal possível de ser gasto, e a possibilidade de uso dos FIIs para isso.

Também podemos ver que o investidor conseguiria simplificar este processo ao usar um FoF ou um multiestratégia, mas, alguns cuidados passam a ser mais necessários. Primeiro, a qualidade do Gestor, pois funcionou muito bem em BCIA11, mas se tivesse tentado com o falecido MGFF11, o investidor teria que voltar a trabalhar.

Segundo, não se pode fazer a trava dos 70% para esses fundos, dada a composição de renda desses, mas usar a trava de percentual do patrimônio. Hoje, passados seis anos desde que eu apresentei o trabalho, depois de muito acompanhamento, estudo e reflexão, eu seria mais cauteloso e travaria o nível de gasto inicial de forma mais conservadora, em 5% ao ano. Mas claro, isso vai depender muito do momento de mercado e da composição familiar do investidor e até mesmo do nível de diversificação da carteira.

O mais interessante desta revisão que eu fiz, foi vislumbrar a possibilidade de usarmos apenas um FoF/Multiestratégia, ou apenas alguns FoFs/Multiestratégia para isso. Quem decide parar de trabalhar, quer simplicidade de acompanhamento e uma estratégia dessas facilitaria muito, e BCIA11 nos mostrou possível, RINV11 tem nos mostrado até que é fácil, mas ainda não temos uma janela de tempo suficiente.

E, para encerrar esse tema, conhecendo você do jeito que eu conheço, deve estar se perguntando “mas se usar a regra dos 4%”, bem, vou deixar você com o gráfico do BCIA11 se tivéssemos usado a regra dos 4%.

Fonte: Desmistificando Research